Rental properties offer tax deductions that other investments don’t. Rental tax deductions help your ROI. However, they still offer monthly income and increased value over time. Before we dig into the tax savings let’s consider what kind of a rental property owner your are.

Real Estate Professional vs. Passive Investor

Are you a “real estate professional” or a passive investor? The IRS has stiff standards for being a real estate professional.

- You, or your spouse, must work a minimum of 750 hours annually in real estate businesses.

- One of you must spend 51% plus of your working hours in real estate businesses.

- You must directly participate in your rental activities.

- As a general rule of thumb, if you have a full time job outside of the real estate industry, you don’t qualify as a real estate professional.

If you are a real estate professional, you can deduct all losses from your rental holdings. As a passive investor, losses are deductible up to 25% of your rental income.

Sources of Rental Income

- Tenant rental payments are income. Also, money collected for the first and last month’s rent is rental income.

- Security deposits are not rental income if they are to be returned to the tenant. If any part of the deposit is not returned to the tenant, it’s income in the year the deposit is retained for a repair. The repair is a duduction. Security deposits used as rent are income in the year received.

- Your tenants may pay for expenses in your absence. For instance, if there is a broken window. The tenant pays for replacement in your absence. This amount is deducted from the rent. This is rental income.

- The tenant provides a service in your absence and the market value is deducted from the rent. The service’s fair market value is rental income.

Examples of Deductible Expenses

- Mortgage interest is deductible. Payments toward principle are not. Expenses incurred in acquiring a mortgage are not deductable. Your mortgage lender will send you a form 1098 that will tell you how much interest you have to deduct.

- Repairs to a rental property are deductible. Improvements that add value are not deductible. Also, improvements have to be recovered by depreciation.

- Travel expenses incurred to collect rent or make repairs is deductible.

- Property insurance

- Taxes

- grounds maintenance

- tax return expenses

- Losses from natural disasters or theft

- Expenses involved with community property if you rent out a condominium.

Record Keeping

- An accurate record keeping system is a must. What do you need?

- You need a record of your rental income and expenses for each property. This will tell you which properties are winning and which are losing. The IRS requires separate records for each property.

- What kind of records are necessary?

- Canceled checks

- Credit card statements

- You have to prove that your deductions are legitimate.

Electronic vs. Paper Record Keeping

Computers take the human error from book keeping. You can eliminate clutter with scanned documents. Scanned receipts have been accepted by the IRS since 1997. There’s a chance of record loss due to system failure with electronic bookkeeping. Data backups prevent data loss. You can back up to the cloud or another off site location.

Paper record keeping is legitimate. It’s best for those who are not comfortable with computers. It saves the time of learning a piece of software. However, it increases the likelihood of error. In addition, you need to retain supporting documents for monies coming in and going out.

DIY Bookkeeping – Is it Worth it?

- To start with, you have to learn another skill, and you’re working on another aspect of your rental business. How much will you get back from the investment of your time? Is it really worth it?

- There are risks involved. What if you miss something? What if you err in processing your transactions? A tax professional works with the information given them. They don’t make sure the bookkeeper is competent.

Pro Bookkeeping – It’s Worth it!

- A quality property management firm will have bookkeeping processes in place. Therefore, they will know what, and how to keep track of it because they make their living doing it. Property management firms will have the needed expertise.

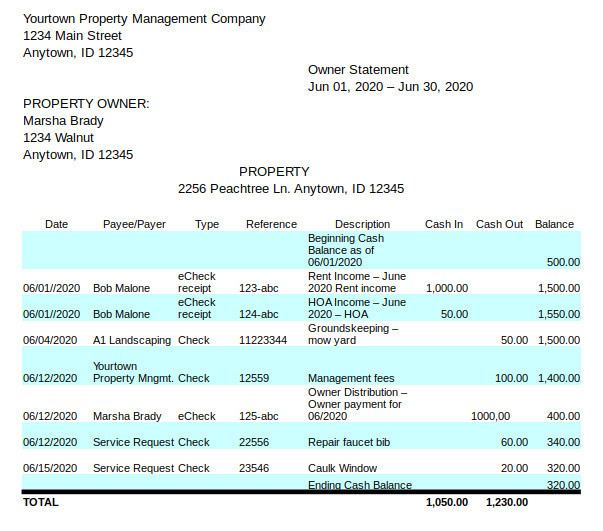

- Jacobgrant can provide the record keeping expertise you need. At the end of the year you’ll get the deductions you deserve. Jacobgrant’s monthly statements are, complete, and easy to understand. Here’s an example with some simple entries.

Think about the time and frustration involved in doing your own bookkeeping. You will do better having jacobgrant manage your properties. Bookkeeping is one of the many benefits of having us manage your properties.

To learn more about how Jacob Grant can improve your Passive ROI with professional bookkeeping services, call 208-795-8218 or schedule a call Schedule call